Double Chin Capital Quant Driven Long Only Strategy

(A monthly long-only strategy replacing Index Trader)

For quite some time we have been working on a low-active (requires a monthly re-balance/position change) investing program that utilizes our stock selection models (that we currently use in Market View). This implementation is a long only portfolio that attempts to outperform the S&P 500 with better risk adjusted statistics. It requires that you trade 12 times a year (on the first trading day of each month) to replicate the portfolio (closing reduced or removed positions and adding new ones). The updated portfolio will be posted 4-6 hours (or by Sunday night for end of months over a weekend) after the close of the last trading day of the month (as the model takes several hours to run).

In the post Covid (current modern era of investing) we have been able to identify some “tells” of institutional accumulation where hands are tipped by using algorithmic execution strategies. The signature of those execution methodologies leaves an identifiable footprint that we are able to detect. By being able to identify the stocks with stronger than baseline/index flow bids, we are able to outperform the index over time.

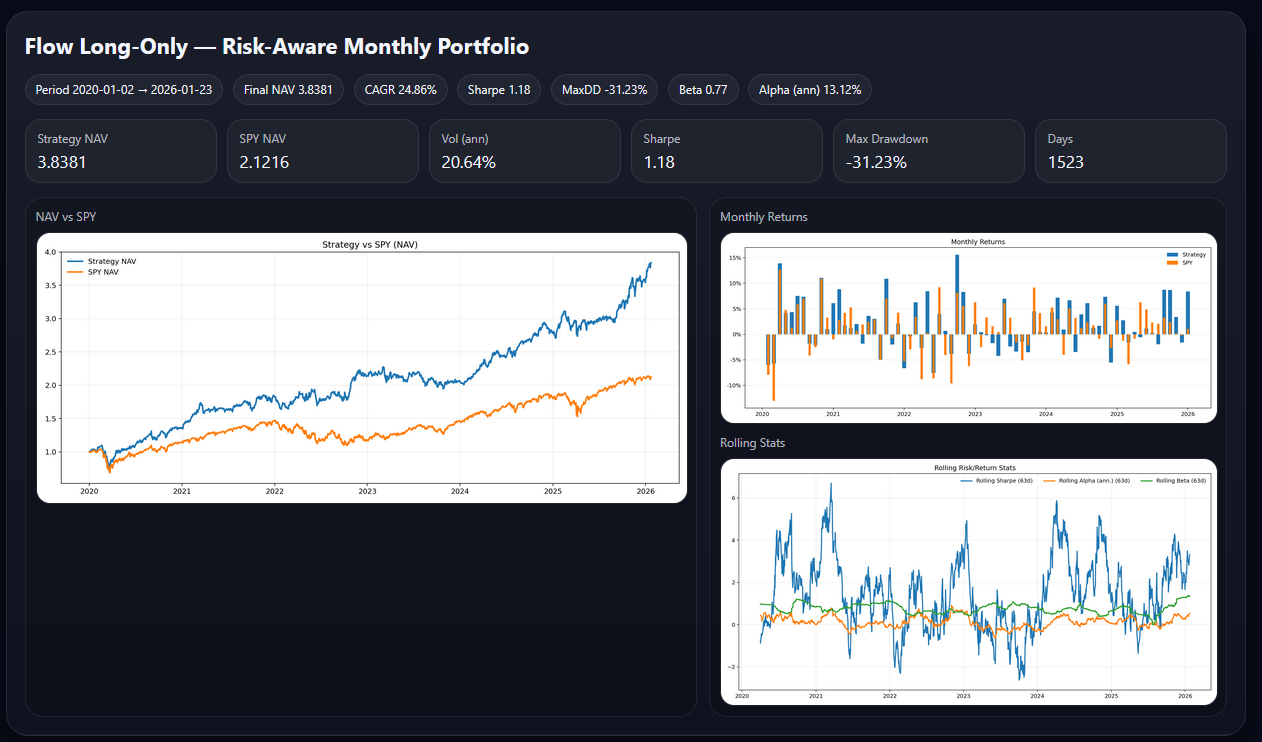

Below is the performance of the strategy from Jan 2020 to last Friday. The model makes portfolio decisions based on the data it has up to the end of the previous month (in this case 12/31/2025). The allocation model is built to maximize the expected risk adjusted performance of the portfolio.

As we look at the portfolio for January 2026 (that was created on December 31st, 2025) we see the holdings and their attribution to the portfolio.

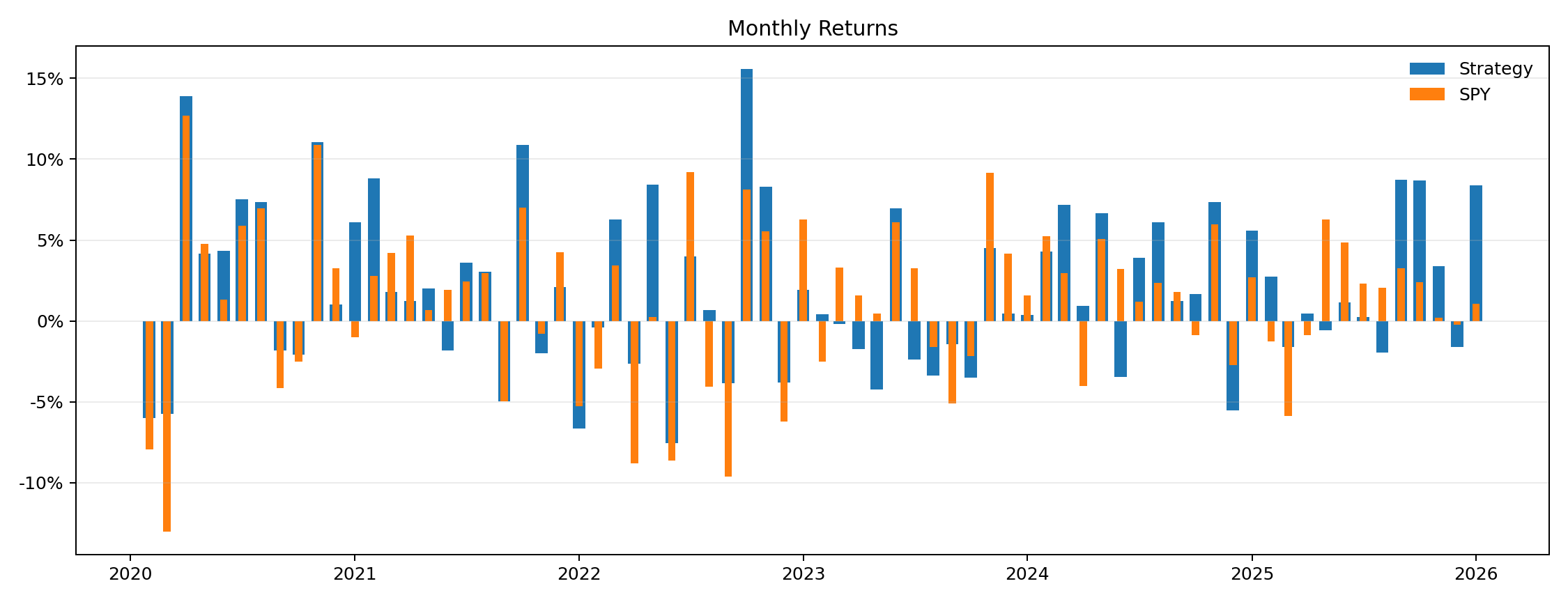

We can also see how the strategy has performed monthly relative to the S&P (SPY).

For our existing Market View subscribers that have stayed with us since the beginning, if you are comped to Index Trader you will remain on a comp for this new product. The first “live”portfolio implementation will be out next weekend (as Friday is the last trading day of the month).

The URL to access the product will be the same for now:

The goal here is to help investors WITHOUT requiring the run a more complicated actively managed long short portfolio. As you can see here this strategy had a 31.2% max draw-down vs a 34% max draw-down for the S&P. Our market view strategy attempts to keep annualized vol MUCH lower than 20% (like 5%) while obtaining an annualized target return of 10%. The market view portfolio is tailored for active and sophisticated investors who are looking to minimize draw-downs and volatility. Our long only strategy is much simpler to implement and is designed for those looking for long S&P risk exposures.

Again, our first live run (with published portfolios) will be next weekend. We would love to have you check it out.

-DCC

When the monthly update comes out does it tell what to remove and add or will we need to look at previous month and compare to new month update?

Love it Chins! Feels like a sleeve of a portfolio not just a portfolio